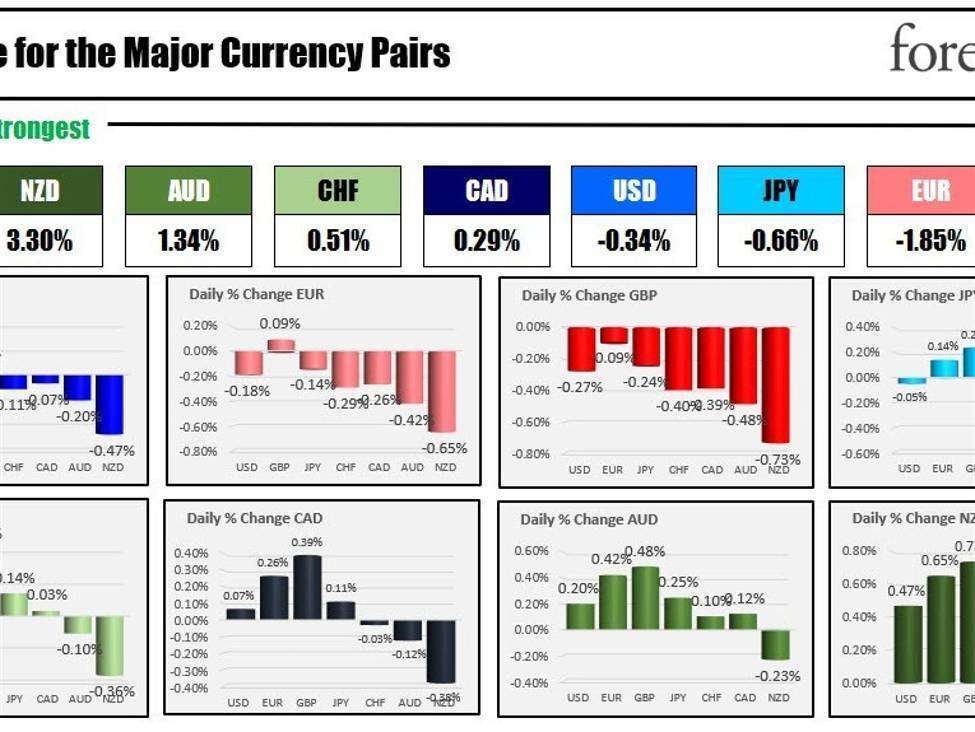

The strongest to weakest of the major currencies

The NZD is the strongest and the GBP is the weakest as the NA session begins. The USD is mixed with the NZDUSD the biggest mover (up 0.47% – lower USD). The GBPUSD is down -0.27% (higher USD). The US CPI data surprised the markets yesterday with a gain of 0.0% for headline and 0.2% for the core, both lower by 0.1% vs the consensus. That sent US yields tumbling, US stocks soaring and the dollar lower. The market is now expecting that the Federal Reserve may cut rates by May of next year. The chance of a cut has increased to 30% for March.

Today the US retail sales report for October will be released with expectations for a -0.3% decline vs 0.7% gain last month. The ex-auto is expected at 0.0% vs 0.6% last month, and the control group, +0.2% vs 0.6% last month. Also released at 8:30 AM ET will be US PPI with final demand expected at 0.1% and YoY at 1.9%. Ex food and energy is expected at 2.7% (unchanged). Business inventories and crude oil inventories will be released at 10 AM and 10:30 AM ET respectively. Canada will release their manufacturing sales data for September with expectations of -0.1%.

Overnight in China data was mostly positive

- Industrial output in October exceeded expectations

- This growth was higher than the projected 4.4% and a slight improvement from September’s 4.5%.

- Retail sales also outperformed, rising by 7.6%, surpassing the expected 7.1% increase.

- The boost in retail sales was largely attributed to the Golden Week holiday at the start of the month.

Beijing’s liquidity measures and a comparison to the previous year’s strict COVID-era policies supported local consumption in October. Despite these positive signs, the overall economic rebound in China remained uncertain, as recent business activity still indicated ongoing weakness.

In the UK today, inflation readings were mostly lower. CPI year on year came in at 4.6% versus 4.7% forecast and 6.7% last month (due to year on year effects). Core CPI came in at 5.7% versus 5.8% expected.

EU industrial production was weaker than expected at -1.1% versus -0.9% expected.

Oil prices are trading marginally lower after modest gains yesterday, which were driven by indications of lower U.S. inflation. The U.S. EIA will release its first oil inventory report in two weeks after a recent systems upgrade. Earlier, industry data from the American Petroleum Institute had suggested a weekly increase of just over one million barrels in inventories.

Stocks are higher in premarket trading today. Target earnings-per-share came in better than at $2.10 versus $1.48. Revenues came in a little light at $25.04 billion versus $25.24 billion. However, guidance of $1.90 – $2.60 versus $2.22 estimate.

A snapshot of the markets as the NA session gets underway shows:

- Crude oil is trading down $-0.21 or -0.27% at $78.05. At this time yesterday, the price was trading at $78.12

- Spot gold is trading up $8.62 or 0.44% at $1971.76. At this time yesterday, the price was trading at $1944.92

- Spot silver is trading up $0.39 or $1.69 at $23.46 at this time yesterday, the price was trading at $22.38

- Bitcoin is trading at $36,217. Yesterday, the price was trading at $36,365

In the US stock market, the major indices are trading higher after prices surged yesterday with the Russell 2000 rising by 5.44%. The NASDAQ index increased by 2.37%.

- Dow Industrial Average futures are implying a gain of 128.30 points. Yesterday, the index rose 489.83 points or 1.43% at 34827.71

- S&P index futures are implying a gain of 20.80 points. Yesterday the index rose 84.17 points or 1.91% at 4495.71

- NASDAQ futures are implying a gain of 115 points. Yesterday the index soared 326.64 points or 2.37% at 14094.38

Yesterday the Russell 2000 rose sharply by 92.82 points or 5.44% at 1798.32

In the European equity markets, the major indices are trading higher

- German DAX, +0.86%

- France’s CAC, +0.66%

- UK’s FTSE 100, +1.17%

- Spain’s Ibex, +0.60%

- Italy’s FTSE MIB, +0.50% (10 minute delay)

In the Asia Pacific market, major indices closed higher after the sharp gains in the US yesterday kick started their equity shares:

- Japan’s Nikkei index, +2.52%. There was a large gain since November 2022

- China’s Shanghai Composite Index, 0.55%

- Hong Kong’s Hang Seng index, 3.92% (largest gain since July 2023)

- Australia’s S&P/ASX index, 1.42% (largest gain since July 2023)

In the US debt market, yields are marginally higher after yesterday’s sharp declines

- US 2Y T-NOTE: 4.850% +3.4 basis points. At this time yesterday, the yield was at 5.039%

- US 5Y T-NOTE: 4.452% +3.1 basis points. At this time yesterday, the yield was at 4.649%

- US 10Y T-NOTE: 4.468% +2.8 basis points at this time yesterday, the yield was at 4.620%

- US 30Y BOND: 4.640% +2.0 basis points at this time yesterday, the others at 4.733%

- 2 – 10-year spread is at -38.4 basis points. This time yesterday, the spread was at -41.9 basis points

- 2 – 30 year spread is at -21.2 basis points basis points. This time yesterday the spread was at -30.4 basis points

In the European debt market, benchmark 10-year yields are trading mixed

European benchmark 10 year yields