The popular movie “Catch Me if you Can” vividly demonstrates how a single individual with the skills to forge checks and falsify their identity can embezzle over a million dollars from US banks. Despite its entertainment value and cult status, the movie also reveals the potential vulnerabilities of the banking system to fraudulent activities.

To prevent such nefarious activities, banks have instituted “Know Your Customer” (KYC) procedures that encompass a range of measures to verify the authenticity of their customers, assess risks, and conduct ongoing monitoring. In this article, I intend to delve into the origins of the KYC process, its objectives, and the challenges that have emerged with its increasing formalization.

Table of contents

Establishing Know Your Customer and Anti-Money Laundering rules

The origins of KYC can be traced back to the 1970s, when the Group of Seven countries established the Financial Action Task Force to combat money laundering. As the use of financial systems for criminal purposes grew in the 1980s and 1990s, governments and financial institutions began to develop measures to prevent money laundering, including the implementation of KYC procedures.

The Financial Action Task Force (FATF) oversees compliance with these standards, with over 200 countries committed to their implementation. Countries that fail to meet the standards are placed on gray or blacklists.

The events of September 11, 2001, prompted the introduction of the Patriot Act in 2002, which updated the BSA and aimed to prevent further terrorist attacks in the United States. Similar legislation, such as the Proceeds of Crime and Terrorism Act, was enacted in countries like the United Kingdom.

Thanks to international coordination, these standards have been adopted globally. As a result, wherever a sovereign country exists, so do KYC and AML regulations.

What problems can be prevented through KYC?

In today’s regulatory landscape, failure to comply with KYC requirements can result in significant fines and penalties. KYC procedures take a risk-based approach to mitigating various financial crimes, including identity theft, money laundering, and financial fraud.

- Identity theft

KYC plays an important role in verifying the legal identity of customers and can prevent the creation of fake accounts and identity theft through the use of forged or stolen identification documents.

- Money laundering

Criminal organizations, both organized and unorganized, use dummy accounts in banks to store funds for illegal activities such as drug trafficking, human trafficking, smuggling, extortion, and other illegal transactions. KYC regulations help prevent them from raising suspicion by spreading the funds across multiple accounts.

- Financial fraud

KYC measures can help prevent fraudulent financial activity, such as using fake or stolen IDs to apply for credit and then receiving funds through fraudulent accounts.

Overall, KYC procedures are an important tool for preventing a wide range of financial crimes and mitigating the associated risks.

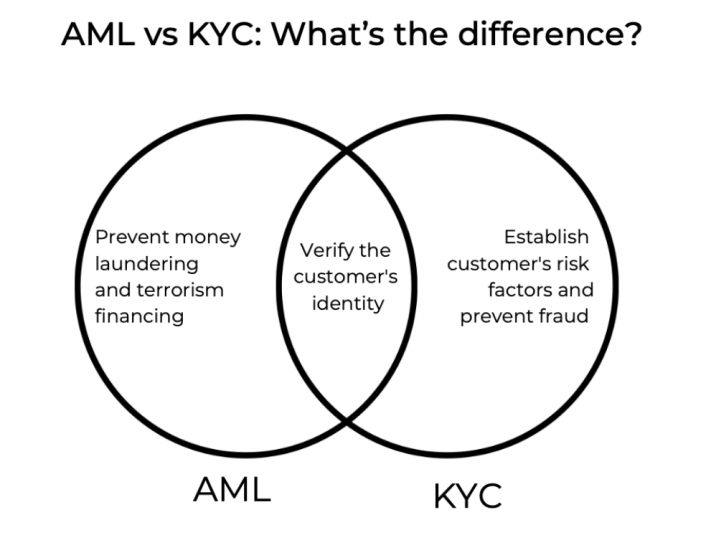

What distinguishes KYC from AML?

AML refers to a set of laws and regulations that financial institutions must follow to prevent money laundering. It includes procedures that banks must undertake to detect and report suspicious transactions, monitor customer activity, and verify the source of funds.

In contrast, KYC is a critical component of the AML framework and requires organizations to identify their customers and verify their identity. KYC processes may vary depending on the financial institution’s policies, but they generally include gathering customer identification documents, verifying customer identity, and monitoring customer transactions.

While financial institutions are responsible for establishing their own KYC processes, AML laws and regulations may differ by jurisdiction or country. This means that financial institutions must establish KYC procedures that comply with the specific AML standards of each jurisdiction to which they are subject.

Overall, while AML and KYC are closely related, they serve different functions in the financial industry. AML aims to prevent money laundering and terrorist financing, while KYC procedures aim to identify customers and verify their identities to help prevent fraudulent activities.

Transforming KYC verification into red tape

The financial services industry is still struggling with the challenge of combating financial crime. Since 2008, regulators have imposed fines of more than $403 billion for KYC and AML violations. In addition, leading banks incur annual costs of approximately $1 billion for financial crime prevention.

However, despite the evolution of KYC and AML processes over the past decade, their effectiveness in combating new forms of fraud remains problematic. While users and businesses have shifted to digital and connected solutions, measures to combat financial crime continue to rely on outdated controls.

Throughout the customer journey, typical issues arise that can affect the performance of financial services. One of the main problems is the presence of fragmented and unverified information, which can lead to inaccurate risk classification and the generation of false alerts.

In addition, customer profiles are costly and time-consuming to review, resulting in backlogs and unnecessary reviews due to inaccurate risk classification. Finally, less than 10% of SARs received by financial intelligence units are immediately actionable by the authorities.

These problems illustrate how KYC verification has become a bureaucratic exercise that creates inefficiencies and potentially reduces the effectiveness of financial crime prevention.

Source: EY

Payments organizations face challenges as they try to meet increasing regulatory requirements and outdated technologies and processes, leading to critical compliance risks and the threat of fines. This leads to a focus on administrative tasks rather than risk management, and the KYC process becomes a bureaucratic exercise rather than a customer review.

How do limitations affect the KYC procedure?

The KYC process is subject to several limitations that may affect its ability to effectively detect and prevent financial crime. These limitations include:

Scope limitations: KYC procedures have a limited scope and may not cover all possible financial crime risks. Sophisticated criminals may use techniques to conceal their identity or funds that are not always detected by KYC procedures.

Human error: the KYC process relies on human judgment and decision making, which can be prone to error and inconsistency. Employees may overlook important information or fail to follow up on red flags, creating gaps in the review process.

Lack of standardization: KYC procedures can vary widely from financial institution to financial institution and country to country, leading to inconsistencies and gaps that criminals can exploit. This lack of standardization can also increase compliance costs for financial institutions.

Technological limitations: technological limitations can also impact the effectiveness of KYC procedures. Outdated systems and processes can affect the ability of financial institutions to conduct thorough KYC checks.

As a result, the focus on bureaucratic procedures and documentation in KYC has reduced its effectiveness as a tool for identifying and preventing financial crime and created the impression that it is a meaningless exercise with little real impact. In addition, the emphasis on compliance and risk management has led to a more rigid and process-oriented approach to KYC that emphasizes customer convenience and comfort.

KYC – really about KNOWING your customer?

In some cases, KYC has been reduced to a bureaucratic exercise that does not serve its intended purpose. This is largely due to the emphasis on paperwork and documentation, rather than financial crime detection and prevention. The extensive documentation requirements have made the process time-consuming and burdensome for customers and have not been used effectively to personalize services or improve the customer experience.

In addition, the emphasis on compliance and risk management has led to a rigid and standardized KYC approach that may not effectively identify potential risks or prevent financial crime. This approach is often inflexible and cannot be tailored to individual customer needs or risk profiles.

Despite the high level of documentation required, the KYC process does not always succeed in detecting fraudulent or criminal activity. There is a story about a former FBI agent who allegedly received payments from a wealthy Russian oligarch to help him “get off the sanctions list“. Therefore, there is a need for greater flexibility and technological advances in the KYC process to improve its effectiveness in preventing financial crime.

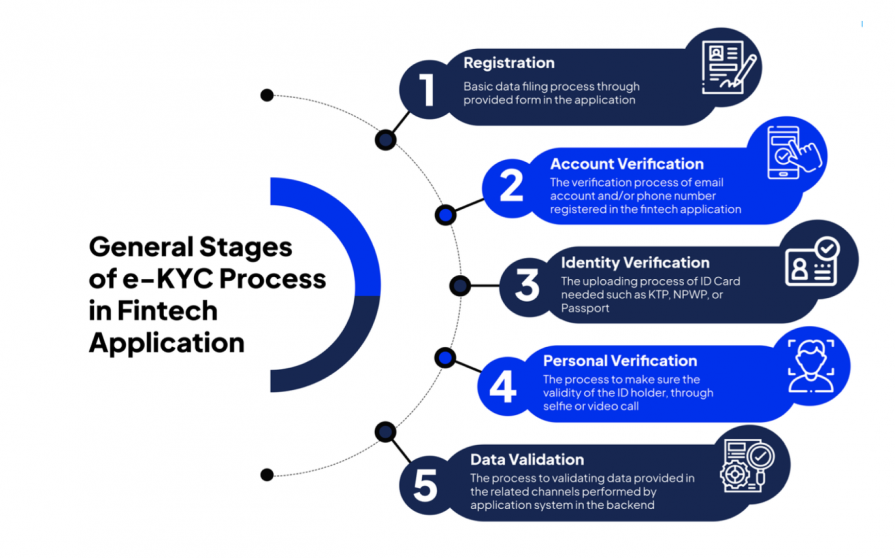

How does KYC improve the verification process?

Despite the threats to the process of user identification, the KYC process counters money laundering through innovative approaches to data collection and storage.

This has evolved as technology has advanced, and many innovations have been introduced to make the process more efficient, effective, and secure.

Verification of digital identity

The use of digital technologies such as biometrics, facial recognition, and AI-powered software has made the identity verification process faster and more accurate. It enables real-time verification of customers’ identities, making it easier for companies to quickly onboard customers.

Hybrid-cloud fintech platform

Save 1 year of active development building on SDK.finance software

Artificial intelligence

AI-powered software makes it possible to automate many aspects of the KYC process, such as risk assessments, document review, and monitoring customer activity. This enables faster turnaround times, reduces errors, and improves compliance.

Data analytics

Data analytics tools are used to analyze customer data and identify patterns and anomalies that may indicate potential risks. They enable companies to identify high-risk customers and take appropriate action to mitigate risk. For example, SDK.finance’s FinTech platform allows you to get a comprehensive overview of each customer’s profile: personal data and documents, accounts, activity logs, transactions and status.

These innovations have significantly improved the KYC process, making it more efficient and secure. As technology continues to evolve, we can expect further advances in KYC compliance.

Conclusion

In summary, the current state of the KYC process is hampered by bureaucracy and outdated technology, resulting in a less effective tool for preventing financial crime. The advent of digital solutions has underscored the need for modernization and a risk-based approach to create a transparent financial system.

FinTech companies must prioritize re-evaluating their KYC procedures, upgrading their technology and operations, and adopting more efficient and effective measures to ensure KYC compliance. In this way, they can mitigate risks, prevent financial crime, and promote a safer financial environment.

Source: https://sdk.finance/exploring-kyc-an-overview-of-the-know-your-customer-process/